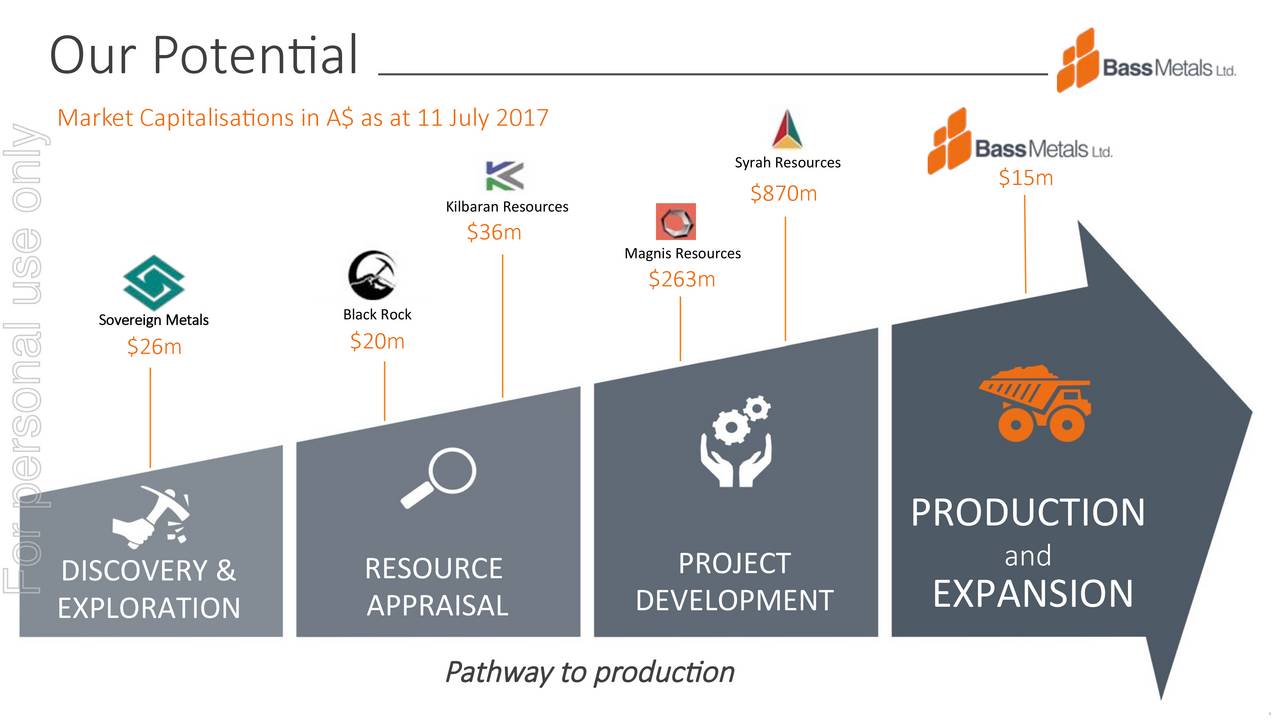

Bass Metals (Official website) Bass Metals - Zero or 100x I am always looking for a good risk-reward ratio. It’s not always easy to find but it is possible. Bass Metals is a large-flake graphite producer that has taken over an existing mine in the tropical island of Madagascar. To make it clear from the very beginning, there is a high chance that Bass will not survive. But I made extensive research and came to the conclusion that I am ready to take the bet. Bass Metal will find additional financing and survive. If this turns out to be true and if other factors play into this bet as expected then it is very likely that the market capitalization will be hundred times bigger than what it is today. And this may happen faster than some investors think. The reason is the following: We are talking about an existing mine. Bass Metals is not an explorer that is drilling some holes for a ‘Pre Feasibility Study’ or some initial 'test drilling'. It’s not a paper dream. The Graphmada mine in Madagascar is operated by Bass Metals and was up and running until last year, after being in production for over 18 months. First, the production was stopped only temporarily due to a period of exceptional bad weather that was expected during the monsoon season . After it became clear that Covid-19 turned into a pandemic Bass metals shipped the remaining tonnes of graphite to its customers and then fired 75% of their workforce.  Monsoon Season in Madagascar What is Bass doing now? Bass Metals quickly decided to go back drilling and therefore expanding their total resources under its control. I heavily support this decision. Graphite prices are still low and there was no point in producing on those levels. But I will explain this in more detail a little later. Let’s jump a step back. Originally, Bass was a gold and base metal exploration company. In 2016 they acquired the above-mentioned Graphmada mine from LSE-listed Stratmin Global Resources and therefore fully moved to Graphite. Bass introduced a new management, completed a capital raising, rebuilt and recommissioned the mine with new equipment and invested into supporting infrastructure like roads and new facilities. Bass Metals has implemented a number of improvements to the Graphmada operation itself. For example they installed a ‘vibrating magnetic separator’. I am not sure what Stratmin used before. The objectives of the work, however, was to increase throughput, recoveries and purity, while reducing operating costs. All mining and processing infrastructure, including roads, bridges, power, camp, tailings dams are in place, along with 40-year mining permits and 20-year landholder agreements.  Graphmada mine in Madagascar Is the Graphmada mine good enough? The main national highway is very close and leads in 110km to the country’s only deepwater port at Toamasina. The mine is soft rock (regolith-hosted) that is characterized by greater than 90% large flake graphite. Large flake graphite (greater than 180 microns) hosted in soft rock allows the large flake to be mined cheaply and processed economically without the use of drilling, blasting and crushing. Graphite hosted in hard rock (also known as ‘fresh rock’) requires higher cost drilling, blasting and crushing operations, which significantly reduces the size of the graphite flakes that are recovered. All hard rock graphite mines have a majority of their production in the fine flake category (less than 180 microns). Fine flake graphite concentrates do not attract the same premium pricing as large flake concentrates due to the unique applications of large flake. The percentage of concentrates that can be produced and sold above 180 microns (large flake) directly impacts the average price received for concentrates produced and sold, sometimes referred to as ‘Basket Price’. The focus is on growing the percentage of large flake graphite production to increase the overall ‘Basket Price’ and therefore the cash margin of the business. Graphmada has consistently produced clean, high purity large flake concentrates, maintaining a 42% large flake concentrate production average, with periods over 60%. Consistent supply of high quality large flake graphite from a low cost mine such as Graphmada is essential to the future of the global supply of specialty carbons, and as such is often referred to as a ‘Critical Mineral’ in strategic supply discussions. Bass metals presented a two stage plan to their investors with the first target at 6,000 tonnes per year and a second phase of 20,000 tonnes per year.  Mining and drying equipment In the first year, Bass modernized Graphmada. There was a wood-fired rotary dryer in place, which dries the final graphite concentrates. Bass Metals replaced that and switched to liquid propane gas (LPG) for heat generation. I don’t know if this saved money but it has significantly reduced the operation’s environmental impact. After the take-over Graphmada transformed into a significant supplier of graphite for traditional markets. And it would be possible to expand into high growth markets as well. On April 4th, Bass Metals announced that they have delivered on all of its Stage 1 objective: Graphmada production highlights to date: ✓ Achieved successful production ramp-up ✓ >96% fixed carbon grade achieved ✓ 42% average large flake concentrate production ✓ Irreplaceable intellectual capital gained ✓ Zero tonnes penalized or rejected to date The market cap at the time of this announcement was 12x higher than today. Although Bass announced at the same day that they will now prepare phase 2 (20,000 tonnes per year) and phase 3 (production of expandable Graphite) some investors realized that something was wrong. Bass didn’t manage to generate a positive cash-flow. And investors started to realize that with those numbers it will also be difficult to do so during stage two. What then followed was the ‘excuse’ of ‘bad weather’ and later the even better excuse of the ‘global pandemic’. In the following months the share price went only south - to AUD 0,002. Other mining companies in Madagascar have been producing all the way through the monsoon and the pandemic. Bass could have done the same. But to be clear, I support the decision of stopping the production and fine-tuning the business plan. What went wrong? In simple words Bass didn’t earn enough money. They destroyed too many of their large graphite flakes during the mining process. Unfortunately, this is exactly where the margin is to gain. When it comes to graphite there are different flakes in the ground. The biggest one are the most expensive and the most rare in the world. They sell for a large premium when compared to smaller flake sizes. Luckily, the Graphmada mine is only one of a very few mines worldwide that can deliver those flake sizes. The quality of their resource is undoubtedly of exceptional high quality. Bass Metals has delivered to various customers all around the world and was never penalized for lack of quality. In fact, the carbon percentage is extremely interesting. I am 100% convinced Bass will have no problem in the future finding more customers and bigger customers for it’s quality graphite. The problem, however, is not the quality of the graphite but the grade in the ground. The average grade of the Graphmada mine is only around 3-4% while in other areas of Madagascar it can go up to 20%. This means that the total mining costs are high - although it's cheap and simple mining without ‘drill & blast’. Bass struggled in its first attempt to make a profit and even struggled to operate with a positive cashflow. Investors quickly turned their back after realizing this. Share price is now at AU$ 0,003 while Market cap has been as low as AU$ 7m. Basically, the venture was declared dead. But I disagree.  Graphmada Mine (Bass Metals)  Mining  Mining Is it really the end for Bass Metals? My opinion is the following: The market cap is extremely low and the stock seems to be totally forgotten or overlooked even from professional investors. Many investors burned their fingers already. Since the stock itself is not even worth a penny anymore, many investors will not even look at it. This is great for new investors. It is the best time to buy stocks when people are too skeptical because of past failures. However, I would like to reiterate my message that this bet only works if Bass Metals manages to stay alive. I started to look at Bass Metals more closely in summer of this year right after I found the market cap down so much. I also spotted some interesting behavior in the chart with volumes up again which made me wonder what is going on. I have covered another Graphite play for many years. The stock is called Talga Resources and their story did show to me that a team with no experience in graphite/graphene can be successful in this sector. What are the differences between Talga and Bass? Talga came from gold to graphite in 2011. Bass came from gold to graphite in 2016. While Talga’s mines are still in early stage the Bass team technically has a producing mine. It's not a paper dream anymore. The market cap of Talga today is 500 million AUD while that of Bass Metals is 5 million AUD. However, there are also some major differences. Talga’s mine is in a tremendous location (Sweden), has the highest grades in the world and some in-house R&D. Bass has very low grades which makes it difficult to be profitable. On the positive side, Bass has very interesting carbon percentages and large flakes. I will explain later why this is so important. And Bass has an existing facility, logistics, and sales channels already in place. Based on only those information mentioned above I would probably still not invest in Bass Metals - even at those low prices. If it is too hard for a company to earn money then we should not invest at all. However, I am speculating on something bigger.  Will there be a graphite boom? I speculate that Graphite prices will increase over the course of the next decade. Prices have been low for almost the entire past decade but have started to rise in the past 52 weeks. If nothing will change with the current battery mix itself we will see an unprecedented demand for graphite in batteries. There is more graphite used in a Lithium-ion battery than lithium itself. Although there are many graphite mines in the world only few have the right carbon mix and are in high enough quality to be a major supplier to this paradigm shift of electrification. Bass Metals graphite is highly suitable for batteries as those two links show: https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2995-01860858-6A822257?access_token=83ff96335c2d45a094df02a206a39ff4 https://cdn-api.markitdigital.com/apiman-gateway/ASX/asx-research/1.0/file/2924-02309601-6A1007423?access_token=83ff96335c2d45a094df02a206a39ff4 My bet will bet that we are entering the ‚Age of Battery‘ and the Western world will need to secure those critical metals. China already controls big parts of the global supply chain. If the West doesn’t want to fully rely on China they do need to build their own supply chain. And it starts by securing big mines that are in operation and capable of delivering high quality graphite. Can this spark a new run for critical minerals? In October 2020, US President Donald Trump issued an Executive Order declaring a “national emergency” to deal with the threat to US security, foreign policy and economy from its “undue reliance” on supplies of critical minerals from “foreign adversaries”—specifically China. In November 2020, the Biden campaign tells miners it supports domestic production of EV metals. In the same month, the European Commission officially launched the European raw materials alliance. And earlier this year, Simon Moore, the Managing Director at Benchmark Mineral Intelligence said: „By 2029, demand for nickel will double, cobalt will grow three times, flake graphite and manganese by four times, lithium by more than six times. The tectonic plates of this industry have shifted." If this is true, this is big.  Graphite If a potential shortage would occur earlier than expected Bass would suddenly find itself in the spotlight again. Bass has a proven track record of shipping quality graphite. The only problem was that the mining itself was too expensive. If Graphite prices go up sharply Bass will be profitable. But still, I wouldn’t invest in Bass based on this assumption only. I asked myself if they can change something in the mining process itself to be profitable even on those levels. Looking into the presentations and announcements it seems that Bass is working on something. Can Bass improve the mining technique? As mentioned above, Bass destroyed too many of their large flakes. The mix between large ones and smaller ones gives miners a basket of different flakes. Eventually, all have to be sold. In the past, they didn’t manage to constantly secure a high percentage of large flakes and ended up with a basket full of smaller flakes. Ironically, quality small flakes are the ones used for batteries. They got all the attention. But prices are still low. I bet that this will eventually change. Now, Bass is looking into a different mining technique. Hydraulic mining is a form of mining that uses high-pressure jets of water to move sediment. I am not an expert on that so I can comment if this is going to work. But if this works, Bass will maybe have very different baskets and therefore very different numbers for their DFS. Therefore, we already have two potential game changers for Bass. Higher graphite prices and the new mining technique. And there is a third one I found. Originally, phase 3 of Bass Metals business plan was to process the graphite in Madagascar itself. The production of expandable graphite. Can Bass go downstream? To produce expandable graphite, natural graphite flakes are treated in a bath of acid and oxidizing agents. Bass could do this for example in a facility near the port and later ship it directly to the customer. This would increase the margin dramatically since the biggest premium is paid for this expandable graphite.  China is growing fast and hungry for Graphite What is expandable graphite? One of the main applications of expandable graphite is as a flame retardant. When exposed to heat, expandable graphite expands and forms an intumescent layer on the material surface. This slows down the spread of fire and counteracts the most dangerous consequences of fire for humans, the formation of toxic gases and smoke. Changes in Chinese and European building regulations and a macro shift towards environmentally friendly products is a driving force behind potential future demand. And the good thing for Bass is only large flakes can be used for this. Demand for expandable graphite for use in flame retardant building materials may exceed demand from electric vehicles. And it’s said that Chinese domestic supply will not be able to meet demand. However, the likelihood of this is difficult for me to judge. If we are very lucky, we will see prices for larger flakes (expandable) and smaller flakes (batteries) go up while Bass even manages to not only sell the raw graphite concentrate but the processed graphite, thus, resulting in a significantly higher margin.  Demand for expandable graphite for use in flame retardant building materials may exceed demand from electric vehicles. Can it go into battery? What we know is that the quality of the Graphmada Graphite is excellent and can go into batteries although in past company presentations Bass did usually target the expandable market more prominently. Even though analysts expected a shortage in Graphite for years - so far only expandable graphite has gone up in price while large flake graphite prices itself have remained rather low. There is one indicator showing this month that graphite electrode prices have hit a 52 week high in China. If true this would benefit the entire sector. But prices are not traded in a central exchange. Usually, it’s a matter of negotiations and buyers are entering off-take agreements with suppliers and miners of graphite. We do have price indications but it is not as transparent as in other commodities. Does Bass have in-house R&D? For a long time Bass has been a pure miner. They managed to take over the mine in Madagascar, modernize the facilities and went back into production on time. They also managed to sell high quality graphite to various customers around the world. What they didn’t have is any in-house R&D team. Or at least I am not aware of that. However, in late April 2020 Bass announced to have signed a MOU with Swinburne University to advance carbon material research and product development. „The combination of the unique qualities of a weathered resource and clean large flake concentrates leave Bass well placed to participate in the development of advanced graphite applications. Swinburne and Bass will seek to explore opportunities for collaborative research activities, including relevant funding opportunities.“ And earlier, in October 2019, there was another announcement from Bass Metals that we will need to look at closer. „Australia-based Bass Metals has entered into an initial agreement with US-based Urbix Resources to develop downstream graphite products. The agreement will see the two companies work over the next six months to set up a joint venture for the processing of high-grade graphite from Bass’ Graphmada mine in Madagascar into value-added downstream graphite products, including expandable graphite. The proposed joint venture will combine Bass’ high-grade large flake resources with Urbix’s environmentally-friendly purification methodology that is not reliant on hydrofluoric acid treatments.“ So I made some research on Urbix. It is hard to find enough information but what I found does indeed look promising. I believe that there will be a time in the future when customers (and car makers) want to have clean graphite in their batteries. The traditional way of purification is not sustainable. This could be a future USP for this Joint Venture. However, Urbix is still a startup and needs to prove that their technologie works for large scale processing. Also, the planned six months negotiation period turned into one year. However, this month Bass Metals announced the following: „Bass has recently concluded a series of advanced tests with prospective alliance partner Urbix Resources (Urbix), a leading US technology firm in the critical minerals and battery materials space that specializes in advanced energy storage cell designs and materials. Bass and Urbix are continuing discussions to establish a critical minerals supply chain for the US energy market, and other technology applications, with test work continuing as Urbix begins to scale up production from their newly commissioned facility located in Arizona, USA. Next Steps: Bass is positioning itself to be a participant in the emerging advanced materials and critical mineral technology sectors, having proven it can produce and sell premium concentrates to specification from its operations in Madagascar. With a well-developed customer base for its premium concentrates, the Company can confirm its concentrates have already been used in the manufacture of specialty carbon products including expandable graphite, nanographite, and maturing graphene technologies.“  Bass Metals What can we expect? The recent development seems highly attractive to me. Although we do not know if this Joint Venture will actually happen, and we do not know the terms of the deal, there is still some potential in Bass Metals. When looking at the quality of the Graphmada resource it makes total sense to me that the team is now postponing phase two of their original business plan. It makes more sense to work on those partnerships and on downstream activities until graphite prices start to pick up. At the same time Bass is, as we speak, expanding its mineral resources, conducting an ongoing and significant drilling program. Numbers so far show again predominantly large flake graphite. Or in other words - more of the same. No positive and no negative surprises so far. The bigger resources does help to underpin a new ‘definitive feasibility study’. And at a later point in time this might help the valuation of the company and eventually the share price when the Graphmada mine is compared to other Graphite mines in the world. In Summer 2020, CEO Tim McManus said in an interview with Chris Brown from ‚Morgan Financials’ the following: „It would make us the largest large-flake graphite producer in the world“  „It would make us the largest large-flake graphite producer in the world“ After this interview I looked at the share price again. I looked at the market capitalization of Bass Metals. With a share price of AUD 0.002 the MC is currently 8 million AUD (6 million USD). There is huge upside for Bass Metals. Considering the low market cap and the existing infrastructure in Graphmada all the Bass team needs to do is to take the findings of their previous attempt, keep drilling and expanding their resource, change the mining technique for the new DFS and move downstream in production. That is what they do and I believe it is possible to make it happen. We are entering the ‘age of battery’ and Bass is sitting on a high quality mine that is up and running. Will this really work out? I have touched a lot of points that may or may not work. And there are a lot of unknowns. Many things need to turn into Bass Metals favor to keep the company alive and to make this mine profitable. But the stock would be trading 10x higher if there are less 'what ifs'. The managing director of Bass Metals is Peter Wright. He is also executive director at the fund management and corporate advisory firm 'Bizelli Capital Partners' in Brisbane. He has been helping with the funding already multiple times and will most likely not let the company down at this stage after taking such a huge bet.  Here is my risk/reward game plan: I believe Bass will get money from Bizelli Capital and/or others. If true --> I believe that drilling results will confirm more of the same quality. If true --> I believe Bass can improve on the feasibility study taking into account the new mining technique and a bigger resource. If true --> I believe there is a real chance that graphite prices will be higher in the near future. If true --> Bass will be back in the game. A big part of the infrastructure is already in place and some sales channels are already established. Where could the market cap be? Market cap could easily be between AU$100 million - 500$ million with more upside depending how the EV story unfolds and depending also where graphite prices go. Bass has a proven track record of delivering high quality graphite. None of their deliveries have ever been penalized. They could be in production in a matter of months if prices allow them to be profitable or if they successfully change the mining technique.  This was a slide from 2017. Bass Metals can compete with all of them and go back into production. There are also other potential catalysts like:

And as always there are a variety of things that can go wrong:

At the end of the day I probably wouldn't invest into Bass Metals at this stage if the market cap is AU$ 100m . Although all points listed above would still be true it's just the risk-reward ratio that wouldn't look interesting. But one should consider those levels Bass is trading now. The 'Age of Batteries' is about to start The 'Age of Batteries' is just about to start with graphite poised to be one of the hottest - if not the hottest - resources in the next decades. Some other interesting developments in the graphite and graphene sector are just about to find the eyes and ears of mainstream investors. I believe it is rare to find a very high quality mine (although expensive to mine) for a market cap below US $7m It's all about risk/reward. If I find 10 stocks with this risk/reward ratio of Bass metals one of them will probably do 100x. Otherwise, I can invest in already established players that will still benefit in the years to come if the battery story should unfold in its full form. In preparation for this research report I have also spoken to some old commodity investors - many of them have never even heard of Bass Metals. One has to consider Bass has only entered the market in 2016. They are not very well known even in the industry itself. Those are fantastic opportunities for new investors that want to participate in a potential turnaround story. One day, Bass will be in the spotlight if graphite prices go up sharply and/or if they deliver on what they are working on right now. In June 2020 Bass Metals raised another $3m million to stay in the business and to keep drilling in Graphmada. Bass said the money will also be used to progress a definitive feasibility study to increase production capacity.  Increasing volume Suspicious moves in the chart

In the last couple of months we can also spot some interesting trading activities in the chart. A sideways channel (From March 2020 until November 2020) is not just going sideways but there are some days where there is (increasing) volume on the buy side. Since the volume is (with few exceptions) still fairly low it does indicate that some speculation is going on. It's not a killer argument for Bass Metals but there might be something building. Is it lasting? We will see. Bass will have to deliver anyways. The increased volumes can be dumb money from people just playing lottery with an almost dead stock or it can be smart money from people that have some insights. This movement does not necessarily need to turn into a spike in the share price - but it often does. Today (24th of November, 2020) - a record volume of 57 million shares have been traded in Australia. Something is going on here. Other interesting considerations: On pitch decks of other graphite mining companies, on those slides on which they compare the different grades of different mines in the world, Bass is never even mentioned. It's like Bass and its Graphmada mine don’t exist. It's literally perfect. Bass is not on the radar of most investors. There is tremendous upside potential for this stock - if only they survive. Update: January 14th, 2021 Since I wrote this research report, two major announcements were made: 1) New screening machines Bass receives outstanding test results from alternative screening process to Stage 1. • Utilizing hard data from Stage 1 production Bass continues to refine Stage 2 studies. • Screening improvements and future availability of hydro-electric power represent significant improvements to the governing parameters of the expansion of the Graphmada Mining Complex. • Bass has begun the search for strategic investment for its Stage 2 expansion for large scale mining and processing operations. https://hotcopper.com.au/threads/ann-efficiencies-identified-for-expansion-of-production.5798780/ 2) The switch to grid power (saves around 30% of cost) The Government of Madagascar’s is progressing a major electrification project between the capital Antananarivo and the port city of Tamatave, electrifying areas along National Road 2, immediately adjacent to the Graphmada Mining Complex. • Upon completion of the electrification project, valued at EUR 203 million, Bass plans to access mains power via the construction of a 20-kV power line from the nearest substation to deliver cheap and clean baseload power to service an expanded Bass’ operation with a materially reduced operating costs. Power was the largest C1 production cost in Stage 1, contributing 47% of operating costs in 2019, equating to $0.30/kWh. Access to grid power from 2024 could halve power costs to approximately $0.15/kWh, effectively reducing C1 operating costs by 30%. The opportunity to utilize grid power allows the Company to consider Dredging or Hydraulic Mining to potentially realize further cost savings for the Project. The delivery of clean power to the Project will provide the added benefit of significantly improving the quality of life in the local rural community surrounding Graphmada. “This is a paradigm shifting development for Bass and its stakeholders, with the introduction of clean energy via hydro-electrification having the potential to significantly reduce operating costs for Stage 2. This has a material impact on the economics of the Project and confirms Stage 2 operating costs will be in the lowest quartile of graphite production globally. The Company will incorporate this latest development into its expansion studies and will align its strategic goal of Stage 2 large scale mining and processing operations with this development." https://hotcopper.com.au/threads/ann-clean-low-cost-energy-for-graphmada.5780750/ Update: January 28th, 2021 I took some time to re-read again the announcements about Urbix Resources: 30th Septemer 2019

26th March, 2020

17th November, 2020

If and when they will announce a potential JV deal to the market we don't know. But it looks as this this is going into the right direction. A reader of my blog pointed out to me that Urbix Resources does have several other MoU in place with other companies or have done test work with graphite. Battery Materials: https://www.asx.com.au/asxpdf/20171219/pdf/43q93ngm3lqstt.pdf 19. December 2017: Offtake agreement & binding test work term sheet and MoU. 10. October, 2019: "The Memorandum of Understanding (MOU) signed by the two companies lays the foundation for establishing the development of a graphite purification facility in Mozambique. Under the terms of the agreement, both the companies will complete all necessary feasibility study work for the proposed JV purification facility." I am not sure about the current status of this relation. Additional research needs to be done. Archer Materials: https://www.asx.com.au/asxpdf/20180905/pdf/43y2k8hc2w21gh.pdf Here I will need to do additional research about the current status of both Archer and the partnerships. To me it doesn't look like it would effect BSM in any way. Renascor Resources: https://renascor.com.au/wp-content/uploads/2019/11/20191118-Battery-Grade-Graphite-Produced-via-Low-Cost-Purification-1999737.pdf 18. November, 2019: So far I couldn't find additional information about a potential JV or any kind of partnership between Renascor and Urbix. I am now trying to check what kind of mine Renascor operates. Update 16th August 2021: Join my Discord for in-depth discussions about Greenwing Resources (before: Bass Metals) https://discord.gg/Qy5GwEYne3 Update 9th September 2021: Last night, I did sell my position due to the recent developments of the company. I believe the renaming of the company was the right move. I also believe the share consolidation was the right move and overdue. However, I am a bit sceptical in regards to the new lithium project in Argentina. Usually a company needs many people with a chemistry degree (as lithium mining it is not really mining). GW1 doesn't have that yet. On the positive side the new resource (San Jorge) is very near to Neo Lithium. I know NLC well since I also wrote a research report about it here. The area there is fantastic, maybe the best in the world. But I don't know about San Jorge itself. Because of that uncertainty I had to exit. Therefore, I did cash-out and will follow the company from the sideline. If there is a good opportunity I might enter it again since I still think the Graphit resource they have is very interesting and even the Lithium resource might turn into something.

7 Comments

Friedrich

24/11/2020 21:05:37

Stunning research ! Well done!

Aat Oskam

25/11/2020 22:30:50

Allready 3 years in my portfolio, wondering why none of the batterymakers or fire-fighting industries are aware of Bass? This fine assessment will help to interest the market I hope?

Nico

20/1/2021 17:17:24

First of all: incredible research! Thank you so much for that!

Never Stop Asking

20/1/2021 18:31:38

Hi Nico. Thanks a lot for your comment!

Nico

21/1/2021 19:38:34

Thank you very much for your thoughts on this and the clarification about the flake sizes!

Ian Olman

12/2/2021 00:28:50

Very impressed with the work and effort that has gone into producing this report.

Never Stop Asking

12/2/2021 10:26:04

"Won't this either cause graphite supply to keep up with requirements so much so that in 3 yrs when phase 2 starts and power becomes cheap supply and demand are likely to be more in sync effecting price paid for the basket." Leave a Reply. |