The Ethereum platform was launched in 2015 and has since become one of the leading blockchains in the world. In fact, it is the second most well-known, after Bitcoin.

Ethereum is often referred to as a "world computer" because it allows anyone to run decentralized applications (dApps) on its platform. Personally, I don't like the wording "world computer" that much. I would rather say it is a decentralized network of computers. This is in contrast to traditional centralized computing systems, where a single computer or server is running an application. By using Ethereum, developers can build dApps that are resistant to censorship, fraud, and other forms of interference, and can be used by anyone with an internet connection. It allows users to "do business" with each other or interact, without a middleman. I'll explain later. Ethereum was first proposed in 2013 by Vitalik Buterin, a young programmer who was interested in Bitcoin but saw its limitations. He proposed building a new platform with a more general scripting language that could be used to build a wide range of applications beyond just digital currencies. Buterin was born in Russia and immigrated to Canada with his family when he was six years old. He became interested in Bitcoin and cryptocurrency at a young age and began writing about these topics for various online publications. Some of the publications he wrote for include Bitcoin Magazine. There, he served as a co-founder and lead writer. He also wrote for the Russian-language website Bitcoin.ru. Buterin also contributed articles to other publications, including the online magazine Hackernoon and the blog of venture capital firm Andreessen Horowitz. His writing focused on a range of topics related to Bitcoin and cryptocurrency, including news, technical, and commentary on the broader implications of these technologies. In 2013, he proposed the idea for Ethereum. Buterin led the development from its early stages and played a key role in its launch in 2015. He has since become one of the most well-known figures in the cryptocurrency and blockchain space. There were a number of other individuals and organizations involved in the founding and early development of Ethereum. One of the key figures in the early development of Ethereum was Gavin Wood. He is a British computer programmer who was the first to get an Ethereum testnet up and running and published the Ethereum Yellow Paper, which served as a technical elaboration of Vitalik Buterin's initial whitepaper on Ethereum. Wood also proposed Ethereum's native programming language, Solidity, and later served as the CTO of the Ethereum Foundation. However, Wood eventually became disillusioned with the centralized aspects of Ethereum's functioning and founded Polkadot. Polkadot is yet another decentralized, open-source blockchain. It is designed to be more flexible and modular, allowing developers to easily create and customize their own blockchain networks to meet their specific needs. Other individuals who played key roles in the founding include Joseph Lubin, a Canadian entrepreneur who is best known and the founder of ConsenSys. The company is focused on building decentralized applications (dApps) and other blockchain-based technologies. One of the most well-known apps they built was MetaMask. ConsenSys has grown to become one of the leading companies in the blockchain space, with a large team of developers in multiple countries around the world. Lubin first became involved in the cryptocurrency space in 2013, when he met Vitalik Buterin, the co-founder of Ethereum, and became interested in the potential of blockchain technology to disrupt traditional industries. He joined the Ethereum project in 2014 as a co-founder and played a key role in the launch in 2015. Another person involved in the development of Ethereum was Charles Hoskinson, who later co-founded Cardano. Hoskinson is an American entrepreneur who first became involved in the crypto space in 2011, when he co-founded the Bitcoin education company Bitcoin Development. Hoskinson joined the Ethereum project in 2013 and played a key role in the early development of the platform. However, he left the Ethereum project in 2014, before the platform was launched in 2015. The reasons for his departure are not publicly known, but it is believed that there were differences of opinion among the Ethereum co-founders about the direction of the project. In an interview with CoinDesk in 2016, Hoskinson said that he left Ethereum because he "could not come to an agreement on the direction of the project with the other founders and stakeholders." He went on to say that there were "different visions for the project" and that he "agreed to disagree and move on." After leaving Ethereum, Hoskinson founded Input Output Hong Kong (IOHK), a blockchain research and development company, and launched Cardano in 2017. Cardano is a decentralized, open-source blockchain platform that is designed to be more secure and scalable than previous generations of blockchain technology. It is focused on enabling the development of complex decentralized applications (dApps) and has gained significant popularity since its launch. In addition to these individuals, a number of organizations and companies were also involved in the founding and early development of Ethereum, including the Ethereum Foundation, a Swiss non-profit organization, which was responsible for managing the early development of the platform, and various venture capital firms that provided funding and support to the project. Some of the firms that invested in Ethereum include Andreessen Horowitz, Union Square Ventures, and Pantera Capital. These firms helped to fund the development of the Ethereum platform and supported the growth of the Ethereum community. So what is the difference between Bitcoin and Ethereum? In very simple words, Bitcoin is like an electronic version of money that you can use to pay for things online. It's kind of like using a credit card, but without the need for a bank to be involved. You can buy things with Bitcoin just like you would with regular money, but it's all done through the internet and with no middleman. Bitcoin was originally created as a digital currency and a peer-to-peer electronic cash system. Today, Bitcoin is primarily used as a store of value. Ethereum is a little bit different. It's not just a way to pay for things, but it's also a way for people to build special kinds of programs and apps that can do all sorts of things. These programs are called "decentralized apps," or "dApps" for short. They can be used for lots of different things, like keeping track of records, or helping people make agreements with each other. All without a middlemen. So, while Bitcoin is mostly used as a way to buy and sell things, Ethereum is used as a platform for building and running these special dApps. Both Bitcoin and Ethereum use blockchain technology to make sure everything is secure and works the way it's supposed to, but they have some different features that make them useful for different things. That's of course just the beginning. There is so much more to say about Ethereum and its entire story.

0 Comments

Hello my friends, and welcome, if you don’t know me, my name is Andrin. I research topics in the blockchain world and present them to you in easily understandable videos on YouTube. And, of course, I will never stop asking. In this series, we go through every single one of the top 100 projects on Coinmarketcap.  ● Bitcoin first appeared in the world in October 2008 in an online forum. ● A White paper was posted by a person or group by the name of Satoshi Nakamoto, he remains anonymous until today. ● The White paper describes the idea and the vision behind it. The title was: “A Peer-to-Peer Electronic Cash System”. ● Every Bitcoin transaction is verified globally by thousands of computers, instead of banks and governments. ● Each time a Bitcoin is sent from one person to another, it is recorded in a public database. It’s called a blockchain. The invention of blockchain technology could turn out to be the biggest innovation in human history since the start of the internet itself, maybe even bigger. To understand Bitcoin, we have to understand Blockchains first. For me, the following example helped the most: In today's world, there are two major things humans exchange with each other:

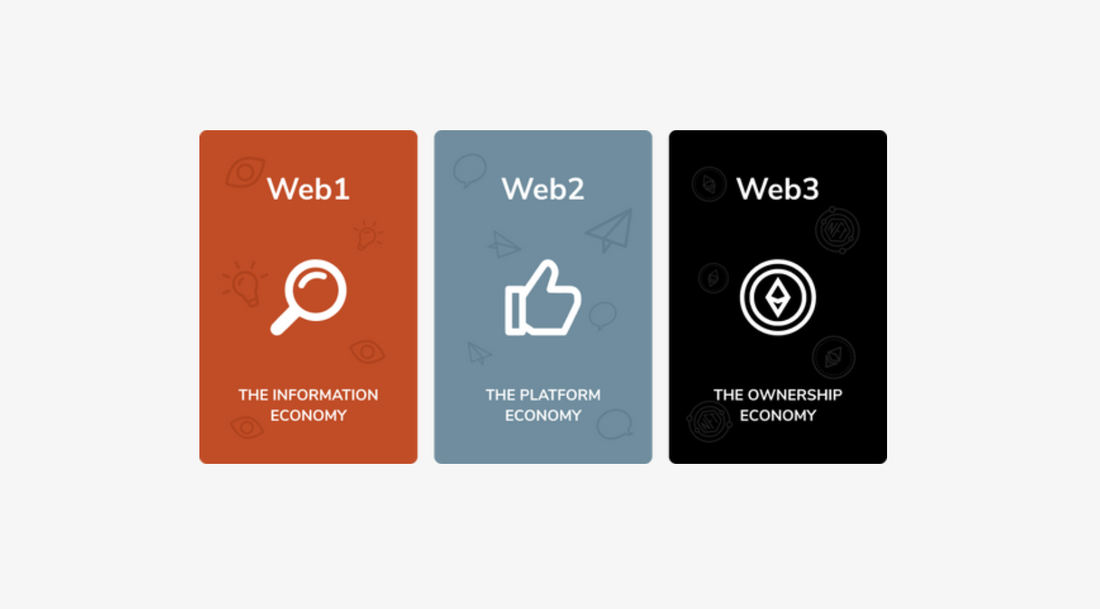

Here is an example: 1. John sends a photo, a text, a video or audio to Peter. Now John and Peter have it. Both can send it to even more people. The information gets copied. All participants have the exact same file. 2. John sends “value”, for example money, to Peter. It better not be a copy. Money can be either here or there. It can’t be in two places at the same time. However, “value” can be a lot more than just digital money. It can also be stocks, options, loans, dividends, commodities, art, contracts, in-game items, real estate, loyalty points and many more examples. The internet is the global standard for the exchange of “information”. But the internet is not very good for the exchange of “value”. Before the internet, we had private networks, like the “Intranet” in a company. Those were already useful networks, because you could send messages to your colleagues, you could share files, you could do many things — but all within your private network. Then, the Internet was invented in Switzerland. The global Internet protocols changed everything, because it connected each and every person on this planet who had access to it and allowed them to easily exchange information. Before that, all those networks were isolated networks, or data islands. However, what we didn’t have for a long time was a global database for the exchange of “value”. This....ladies and gentleman... is where the blockchain will change the world. Up until this time the world needed to rely on middlemen (like banks) to exchange value, as it wasn’t easily possible to keep track of value ownership collectively, globally and securely. Think about the thousands of banks that exist today. Think about Paypal, Wise, Revolut, stock brokers, stock exchanges, Visa, Mastercard, and all the players in the finance sector. It used to take days to send money from one country to the other. They all operate their very own databases for value and track all the users’ funds in their own data islands. They are now connected through something called APIs with some other players in the industry so the person can send some kind of “value” to someone else. Sounds complicated? It is. That’s why everything takes so long and is so expensive. Now, think about all the other digital value that is out in this world, but is not at all connected to anything. Digital art, digital in-game asses, loans, even digital loyalty points. Imagine a world in which there would be one single global database, but not for information, but for value. Imagine this one big global bank, which is not controlled by a company, but by millions of people just like me and you. This is the potential of blockchains. At its core, Blockchain is nothing else than a public database, the new global standard that enables the exchange of “value”, just like the internet was the global standard for the exchange of “information”. It will make the exchange of different kinds of value a lot faster, cheaper and easier. This is Web3. This is a revolution. Not now, but in a few years. Now, let’s go back to Bitcoin: Bitcoin was the first use-case of a Blockchain. It was the first time you could send some kind of value or money from point A to point B, without the use of a bank or without the need to trust a middleman company. This doesn’t make Bitcoin good or bad. And it doesn’t tell us if Bitcoin will go to zero or to a million. But it’s important to understand the technology behind it. The Bitcoin Blockchain went live in 2009 Based on the Whitepaper, it was intended to be digital cash. Today, people see it more as digital gold and not as a currency in the traditional sense. The reason for this is that there can only be 21 million coins. People started to speculate, kept the Bitcoins, instead of spending it. Historically, humans and governments have been fairly bad at creating money. Theoretically, governments can print endless amounts of money, and most currencies don’t survive more than 100 years. Some people believe in Blockchains, but not in Bitcoin. Others believe in Bitcoin, but not in any other cryptocurrency out there. And yet others are convinced Bitcoin turns into some kind of settlement layer that the world trusts. Personally, I don’t know. I am Swiss, so I am neutral on this. But I think it’s worth reading and learning more about it. In the next episode, we will look at ETH and the Ethereum Blockchain. The second biggest project out there. Having said that, I wish you all a great rest of the day, to the moon, and... Never Stop Asking.  In Web3 we need to stop thinking in terms of products, and start thinking in terms of economies, because a Web3 startup does not generate sales from selling products and services, it generates revenue from… (read the full article to find out what it is). In this article, I would like to elaborate on four main topics that are deeply connected to each other: 1) Digital connection, reputation, and ownership 2) Blockchain in simple words 3) Middleman companies and trust 4) Web2 vs Web3 companies But first, let me start with an introduction: We spend easily about 50% of our time awake looking at digital screens. The physical world and the digital world are melting together more and more. Although people try to actively reduce screen time, the reality is that even with less screen time, we will be even more dependent and connected to the digital world. This trend is growing, has been growing, and will be growing for a long time. Whatever we do on the internet and whatever we post, we are creating something I call a digital reputation. We are leaving behind a digital trail. In Airbnb, your digital reputation is what people actually trust when they decide to host you. The consequences of bad reviews might be that you are not even allowed to stay. Your digital reputation can get you a date, but more drastically, it can fail a potential date before it starts. Who can resist the temptation of quickly scrolling through the public information and images of the other person? A solid digital reputation is also what might land you a well-paying job, assuming the human resources department successfully checks your public social media channels and doesn’t find a red flag during the deep dive into the Google search results. Over the last two decades, we all have been building a reputation in the digital world, whether we wanted it or not. We are constantly making more connections with people, companies, and to so-called online knowledge sources. Imagine you meet a new person in a co-working space, during a business event, or anywhere in your life. You meet him physically, shake hands, and then exchange the contact details for the digital connection. But more importantly, right after you separate again, you will probably take a quick look at his profiles, his LinkedIn, Facebook, and google his name. Your digital identity, your digital data, and even more important, your digital reputation is slowly becoming more important to you than your physical one. But ask yourself, when everything depends on your digital reputation and your online connections, the one question you need to ask yourself is: who owns it? An average internet user has 150 different accounts. Yet, you own none of the data. Even with GDPR, the general data protection regulation from the EU, you still own none of the data. Now it is time for a thought experiment: Imagine you lose access to your water supply in your house. Most likely you will buy some water elsewhere, get it fixed, and continue with your life. What about when your power connection breaks down? Same story, eventually, you will somehow get it fixed and then just continue with your life. But what about if you lose your digital reputation and all your online connections? The reality would be devastating. You will almost need to rebuild 20 years of the reputation you created over that time and will have to make all the connections once again. All the creative content you created over the years: lost. All the followers and subscribers: gone forever. It is one big illusion that we are in control of our digital life.  Who owns you when you’re logged into your computer? Who owns your data when you are building your reputation online and connecting to all the interesting people, companies, profiles, blogs, and knowledge sources? If you spend half of your life in the digital world, but you don’t own what you have built on the internet over all the years, then half of your life is not yours. This is happening because in today’s world all the data is on centralized databases, owned and operated by corporations, not by you. There is a systematic risk for each and every one of us who stands for a free and open world, and this is where blockchain and Web3 can make a huge difference. Blockchain in simple words At its core, a blockchain is nothing else than a database. It is a public ledger. Imagine an Excel sheet that is open for everyone to contribute. However, a blockchain is not owned by a single company or a person, it’s owned by millions of people across the world whose personal computers verify each transaction or each new line that is added to this database. Essentially, a blockchain is a ledger of digital transactions. Every person with an internet connection can add data to the blockchain, but no one can manipulate it. If you want to change the data, you’ll have to send a new transaction, which will add a new line to the database, and that will connect to the previous one. All transactions will be bundled into blocks, cryptographically secured, timestamped, and connected to each other. If someone tries to manipulate any parts of the database, the other 99.9% of computers will realize that something is not adding up and won’t allow it to happen. This feature, and a cryptographic part of it, makes the blockchain very secure. This was a very simplified explanation of blockchains and there is a variety of different blockchains with very diverse specifications. To better understand why blockchains are such a groundbreaking innovation, let me give you a bit of background about the history of the internet. It all started with something that is now called Web1. In the 1990s, websites were rather static and, from today’s perspective, visually not very appealing. People accessed websites mainly to find basic information. It was more about replicating the information of the physical world to the new digital world. Many websites functioned like business cards, containing some core information like address, phone number and opening hours on their homepage. Then, around 15 years later, for the first time users could easily create and upload content online — from text and images to videos. This phase of the internet is considered Web2 now.  Facebook and other social media platforms started to gain momentum. Users connected with other users, followed and subscribed to each other, and started to build something like a reputation in the digital world. Web2 essentially allowed people to connect and create communities. It allowed them to be digital creators and create the multi-billion creator’s economy we know today. But, again, the one question you need to ask yourself is: who owns the data? The short answer is, to no surprise, the big tech companies. There is this famous saying that if you’re not paying for a service, you’re not a user. You are the product. Companies profit from your data with their private database. They monetize the traffic and attention that you generate for them. In return they give you little to nothing. Although it is not a secret anymore that tech companies have become slightly too powerful and earn money off of our content, most people are not aware that there is a solution. This is where Web3, Bitcoin, Ethereum, and blockchains come into play. Essentially, Web3 is about digital ownership. And with digital ownership countless new possibilities emerge. Instead of being a passive user on all those websites and platforms, blockchain technology allows people to become something like their very own tiny little micro-company that owns their data. We can all own our content, our posts, and our identity. We can allow others to make use of our data and generate us money, just like the big tech companies have been doing it. We have the potential to build a world in which we really own our data, reputation and our connections. And of course, it will not be rocket science to transform yourself into your own micro-company and to allow all this to happen. My prediction is that in most cases, it might require just a single click. It might become the new normal.  For the next part of this article, I’ll talk about why blockchains have so much potential by explaining two very important concepts: information and value. I have also written about blockchain’s potential in a previous article. Feel free to check it out here Technically, there are two major things humans exchange with each other: - Information - Value The main difference between information and value lies in its functionality. One can be copied, the other can’t.

The Internet is the global standard for the exchange of “information”. Before that, we had private networks, like the “Intranet” in a company. Those were already useful networks, because you could send messages to your colleagues, you could share files, you could do many things — but all within your private network. It was the global Internet protocols that changed the game because it connected each and every person on this planet who had access to it. Before that, all those networks were isolated networks — or data islands. However, what we didn’t have for a long time was something like a global database for the exchange of “value”. This is the blockchain. Up until this time the world needed to rely on middlemen to exchange value, as it wasn’t easily possible to keep track of value ownership collectively, globally and securely. Think about the thousands of banks that exist today. Think about Paypal, Wise, Revolut, stock brokers, exchanges, Visa, Mastercard, and all the players in the finance sector. They all operate their very own databases for value and track all the users’ funds in their own data islands that are connected through APIs with some other players in the industry so you can send the value to someone else. However, not everyone and everything is connected. The solution would be a public database that enables the exchange of “value”, a new standard that secures our privacy and allows every person on the planet to participate. It must not be controlled by a single person, a company or organization. This is what a blockchain is. Instead of connecting millions of data islands through APIs, people will just connect their back end to a blockchain. This technology will have implications on our lives as big as the ones created by the invention of the internet. Let me give you one more practical example: Think about a digital advertising banner at the top of your blog. It could also be considered “value”, because it can generate money. The reality is you don’t really own the post, and you don’t even own the advertising space. In EventScouts, the web3 Startup we are building right now, you will be able to own your post as well as the ad banner, trade it, and earn money with it. There will be no middleman like Google Adsense in between who takes a hefty cut. Essentially, we give power back to creators, as we try to connect ad banners to the blockchain and make it tradeable and exchangeable with all the other values in the blockchain ecosystem.  About Middlemen companies If we analyze all the fintech companies mentioned above in this article, we should realize that they offer nothing else than what is called a middleman service. The goal of sending money from point A to Point B is to deliver it to Point B as fast and cheaply as possible. It is not the goal for the end user to go through the hands of a middleman service like a bank or Paypal. As humans, we just accept these methods today because we didn’t have a better solution — until now. Such middleman services don’t add much value to our world, and there are costs of running those trusted third parties. They create a tax on the entire society. Blockchain will be the solution to this problem, because it allows peer-to-peer transactions, in other words, it allows transactions from people to people directly. It literally removes the middleman company. Web3 is a revolution in how we exchange value with each other and how we are looking at and how we are managing trust. But let’s quickly look at why trust is so important People will only buy goods and services from each other if they can trust each other. Naturally, we do not trust each other as human beings. So, over the years we started to create governments, systems, and frameworks and most importantly we created companies. Before Airbnb, it would have been absolute madness to let a stranger sleep in your house. Airbnb completely changed the game. The reason for this is, that you don’t trust the stranger, you trust Airbnb, the middleman company. The tech company Uber is actually only connecting two users, a driver who looks for a passenger and a passenger who looks for a driver. They use their own central database to store and manage this data. Again, hopping into a stranger's car was unthinkable only a decade ago. The reason people do it is because they trust Uber and the digital reputation of the participants in the application. Web3 can make this method of having to trust a middleman company obsolete. Some blockchains come with something called smart contracts. Basically, smart contracts are programmable code that executes itself on a blockchain. In other words, it can connect those two parties mentioned above in the Airbnb and Uber example automatically, without the interaction of other humans. Smart contracts are capable of handling everything from bookings, and payments, to ratings. Parts of the core business of tech giants like Google and Facebook, who both earn a lot of money through collecting data from users and selling it to advertisers, could technically be replaced through different blockchain applications. A big part of their business is the digital middleman business. Imagine the advertising business model, where on one side is content and traffic, and on the other side are businesses who want to have exposure to it.

Now, for the last chapter, let’s look at the economic side of things: We already know who owns our data today. Big tech. Now, let’s see how Web2 social networks earn money, how it is different from Web3 and what trends we can see in the industry. Web2 social networks build platforms that let users create content and generate traffic to their domains. The revenue comes either from businesses or from users. They are allowing users to build communities but don’t allow them to be truly the owners of their creations and connections. If the platform dies, so does the content. If they want to censor you, they have the power to do so. Users get zero percentage of the monetization that Facebook and other social media platforms are making off of them. The one and only reason some platforms like YouTube redistribute a tiny percentage of their revenue to the users is to motivate their power users to create even more content that they don’t own. Ten years ago, Facebook was the ultimate undisputed center of social activity on the internet. It had literally a monopoly. Ten years later, we are having our own digital spaces for very different environments, for example, work environments, leisure, social activities, education, gaming and much more. Let me explain: most apps have some kind of social part built in that allows you to connect, subscribe and contribute. Finance apps let you follow other traders. Book apps let you follow interesting Authors or other readers, and travel apps let you connect to people or content you may like. We have dozens of apps on our mobile phones for all of our interests, and we joined multiple social networks even if they don’t feel like social networks. People even use multiple Twitter accounts to follow both, work-related content creators and hobby-related creators. There is a clear trend towards more social connectivity across more platforms. Facebook is losing active users, and new social media platforms are popping up in all shapes and forms. Our connections, which are built on our reputation, will continue to grow in the digital and virtual world and transform into something that is currently called Metaverse. Maybe best described as a place that merges the physical world and the digital world. Blockchain will give ownership of the data to people. Users of the internet should own their data, and deserve to earn money with it. The future is to let people collaborate directly with each other, through the use of blockchain technology. Web3 will create a decentralized environment in which a user can do transactions and interact with another user, without the need of a middleman. Imagine the long-term implications this may have to our society if countless Web2 companies become obsolete, simply because users can send money and value peer-to-peer. This also means that Web3 startups are fundamentally different from Web2 startups because we are not offering products or services to end users or businesses. Web3 startups are creating economies and the tools to allow people to interact with each other directly, peer-to-peer, through smart contracts. The token holders, the owners of those smart contracts, collect a minor transaction fee. That’s where the value is. A smart contract is not bound to a single website, a single platform or a product. There can be multiple websites, multiple front ends, all connected to the same public database, the blockchain. A Web3 Startup can and should grow into an online economy, not into a company. It is part of a much bigger decentralized ecosystem. New decentralised social networks in the creator economy will probably reach mainstream attention only in a few years. Rewarding users with ownership can help attract enormous user bases that have the potential to outcompete the existing, centralised counterparts. The reason for this assumption is that ownership for end-users eliminates the conflict between the centralized company behind a social network and the participants, the end-users. It ensures that all stakeholders (investors, users, businesses) are better aligned. In Web2, platforms strive to earn as much as possible, while users want to discover relevant content and information. This misalignment is dangerous. Because of network effects and because of the lack of ownership, it is hard for end-users to leave a social network for a better alternative. This all could change if the user is in possession of his data. We see the job as a Web3 platform to provide the users with the means to transact with each other in a secure and trustable way, not through us and our central database. We create the tools and frameworks that allow users to create and own the assets and then trade them with other users directly. Web3 is not about selling products or services. It’s about creating economies. The smart contracts that power those economies will collect a part of the value that is traded in those economies. And those decentralized economies could grow much bigger than everything that we can imagine right now. If you enjoyed this article please also DM me and let me know your thoughts. My name is Andrin, I’m the founder of EventScouts. I’m here because we are building a blockchain protocol that will allow users to upload information (in our case lists containing activities and events) to a shared database, the blockchain. The content created by users will be owned and controlled by the users, and allowing them to earn money with it directly. It basically is the first blockchain based, user-owned, event and activity database. event-scouts.com *** This article is also on LinkedIn Here is my Linktree  This new system would revolutionize not only the education sector but our entire society. Today, I am more convinced than ever that this system will lift the human potential across all classes, simply because there are more incentives for people to help each other. Having said that, society would also need to counter the flaws in this new system by implementing new laws and regulations. I believe this is part of every major transformation. The problem

The solution Let me explain this new system again in a very simplified way: People would be seen as their own company. Its shares (tokens) are traded publicly and entitled to “dividends”. The dividend is paid annually. It can be viewed as an “education tax” and is calculated based on the annual income of that person. Let’s say it is 1% of the salary. It could also be 0.1% or 2%. The tax authorities will collect this 1% tax through ordinary taxes and redistribute it to people (shareholders) who educated and supported the person over all those years. Those shareholders are mainly teachers and mentors but can be anyone who believes in the person. Now, we have already created financial incentives for people to help each other, because you can get a small part of someone’s future salary. However, I am not only looking at teachers here. Many people will suddenly have an interest in helping you. All this will be on the blockchain — a shared database — so that everyone can connect to it. If we program it in a smart way then we will create an open, transparent and fair incentive system that brings society a step forward.  Practical examples To keep it accurate, I replace the word “share” with “token”. Tokens actually represent value or utility on a blockchain. The dividend is of course not a dividend in the traditional sense but represents a right to a payout based on programmed parameters — in our case a part of future salaries. For every child who enters the school system the government launches its very own token. Imagine your child is called John Doe. He will soon go to school. The government will create the “JohnDoe Token” and issue 100 JohnDoe tokens. Those 100 tokens represent 1% of your future annual salary — every year. On day one — the day of the launch — the government holds 100% of the tokens. To set the incentive right, teachers directly working with John Doe will receive some JohnDoe Tokens from the government and therefore participate in the future success of your child. We can discuss and agree about how many shares teachers should receive. Should only the teachers with direct influence on the child’s development get shares? Or the entire team? Or we can discuss other parameters: Like the amount of tokens to be distributed, the time-frame or the impact a certain teachers needs to have. The goal must be to have a fair system with the right incentives for the people working in the education sector to put maximal effort into educating your child. Over the years teachers get free tokens distributed to their personal wallets as part of this new incentive system. This can be seen as a way to say “thank you” to teachers and might make a little or big difference in their life. When John grows up and starts working, 1% of the salary will now flow back to all the token holders. But this is only a simplified example. In all the years many people could acquire tokens of John — because it is a free market. Friends & family, a neighbour, a coach, or just anybody who believes in John. Those people have no “rights” about John itself. He is not required to do anything for them or meet them personally. But token holders will get a cut of his future income.  The market price The tokens are publicly tradable on the blockchain. They might appear on different websites. Because of that a real market is forming. There will be no problem regarding the liquidity on the order book to buy and sell those tokens, because in the last few years Bancor invented a new mechanism. You can find out more here: https://support.bancor.network/hc/en-us/articles/360031143851-How-Is-Bancor-Different-than-a-DEX- In his class, John emerges as a clever student. People close to John and people in the education sector and so-called new “educational venture capital funds” recognize this very early on and buy some JohnDoe tokens. Technically, there is an annual dividend which will probably last for +45 years — all the years John works. The token price itself will peak at a certain time because of the time factor and the total expected cash flow which will sink as John comes close to his retirement age. If the token price is too high it will be more lucrative for investors and mentors to buy tokens from Peter who might not be as smart as John, but is also expected to land a good paying job. Alex on the other hand is struggling a lot in school and in life. His family is rather poor. The token price of Alex is still extremely low because it doesn’t look like he’s going to be a top earner in the future — unless he makes a big personal development. A person close to the family wants to help Alex get back on the right track. This could also be a teacher, a neighbour, a VC, or just anyone. This person realizes the potential of Alex, buys shares and supports him as a mentor. Maybe he provides him with free tutoring, buys him computer software for new ways of learning, helps him with his personal network of people and opens up new visions and possibilities for him. Now the token of Alex appreciates because other people also realize the personal development Alex is making and therefore participate in his success.  A new form of VC’s The so-called “Educational VC’s” are probably crucial here. They are something new which doesn’t exist yet. I compare them to scouts in sports or VCs in the start-up sector. They pour money and resources into students who have not yet reached their maximum potential — because that is where the greatest return is to be found. In the startup sector, if the market price for a startup is too high, it will not be attractive to invest into them because of risk/reward. In our case, if they find students with a market price too high, they will not invest and look for students with a lower market price. Those students might be underrated. They are exactly the ones which need the most support. VC’s or mentors will invest resources (time, money, network) into them to make that positive change happen and unlock the full potential. Most money will therefore be invested into students which have not reached their full potential yet. While for top students the token price might already be so high that it makes financially no sense to invest — unless you believe your mentorship will make him even more successful. Therefore, this market mechanism sets the incentives just right and creates a fair system of people supporting other people.  Sports, Music or Comedy In addition, this new system of “tokenizing the human potential” would not only apply to schools or the education sector in the traditional sense. If a mentor or investor realized that someone has talents in sports, music or comedy the market would realize this fast and will price it into the token price — because now there is a probability that the future earnings will be high. Investors jumping in early will most likely provide the person with great support — because they have an incentive to do so. This could again be mentorship, access to the personal network, ideas, mental support, resources or just anything positive. Money flows An interesting aspect is the flow of money in this new system. The government issues the tokens and guarantees the dividend by collecting and redistributing the tax through the blockchain. Once the government allows the tokens to be traded publicly, and there is interest from someone, the money flows from the private sector to the government. The government now has the opportunity to redistribute the money directly to the school of the student, therefore creating even more incentives for all people on the frontline of education to help students as much as they can. In the smart contracts many more incentive mechanisms could be programmed. Ultimately, a whole new incentive system could finally emerge in the education sector and one which lets the entire society collaborate. It is meant not only for teachers but also for private mentors or supporters. Because the power of people helping each other is everywhere — it’s just not fully unlocked. Maybe at some point ETFs will be created that will invest millions of dollars into a wide range of tokens that represent and support a certain group of students. Due to the market mechanism, the incentive for certain mentors or investor groups would be gigantic to turn bad students into good students — or even bad schools into good schools because that is where the greatest return could be found. This market price mechanism sets the incentives for people in a way that makes it most lucrative to help the weakest the most. In general it can be said that depending on how big the financial incentives effectively will be it can make a big difference in the lives of many people because now people have more than one reason to help each other. Even if the return is years away or fairly small, it’s worth it — and it is the right thing to do. I believe a wide range of financial products could be created to facilitate the industry even more and therefore pour even more money directly into the education sector and directly to schools. There could be billions of dollars flowing in from the private sector into the education sector in a very targeted manner and fully transparent — which is great to counter corruption in this sector.  One more idea: Years later, students or ex-students could reward their best teachers, mentors or any influential people in their lives with their own shares and therefore automatically distribute a part of their “education tax” to the people who actually deserve it the most. All parameters can be programmed securely and transparently in smart contracts. For example, you could program that 1% of new shares are created annually, which people can only transfer to teachers who already own your shares. Therefore, students a few years after they left school could look back at life and choose the best teachers / mentors they had. This is only an example, the possibilities are absolutely limitless about what we could program into the smart-contracts to create a working and positive incentive system. The distribution of the actual money on the blockchain is anyway fully automated, so there is no risk that the government will lose, delay or mess up payouts.  At the end, I believe it boils down to one core question: Do we want a system in which people have financial incentives to help each other? Or do we just continue like we have done for the last hundreds of years.  I believe the education system worldwide needs to radically change to unlock the full human potential. What about we let teachers and other mentors participate in the success of their students? Imagine that the identity of each child is registered on the blockchain and automatically launches its own token as soon as it enters the government’s education system. Now, all teachers and other people working closely with the child will periodically be rewarded with a certain amount of the child’s personal token. Once the child turns into a young student and finally grows up and contributes to the economy it’s time that teachers and mentors will get back a reward. A tiny percentage of the salary can now be distributed back to all the people who had a significant effect on the students personal development and skill shaping. This will create a long-term financial incentive for people working in the education sector as well as for other members of society who are ready to help young people become successful.  Personal token We can push this thought experiment one step further. If every human will have its own token that is tied to his very own economical success, then we can even give it a market price. In school it will already become clear which students have acquired the necessary skill set to succeed in the education system and will therefore most likely earn money in the future. On the other hand, some students might get on a bad path and it is possible that they will eventually need to be supported by taxpayers money. Therefore, the token of successful students will appreciated in anticipation of future success — just like a stock of a publicly traded company does. The token of a less successful student will be traded on a discount. This creates tremendous opportunities for teachers, mentors and investors to jump in, buy more of that token, and provide extra support in all areas needed. The biggest supporters It’s possible to change young people’s lives if only they are surrounded by the right people, have access to the world’s intellectual resources and over time create a positive attitude, hope and believe in a better future. If an investor now scouts hidden talents or sees potential in any kind of skill that the society appreciates, he can directly invest in the token of this young person and therefore directly participate in the future success. Not only that, I believe most investors would turn into the young people’s biggest supporters since they will also be financially rewarded later on. An investor can choose to buy tokens from top students but will have to pay the premium since the possibility of future economic success is high. Through this incentive system, I believe hidden talents in students from all walks of life will get discovered a lot earlier and a lot faster and will be boosted through direct support of teachers, mentors and investors. Society will greatly benefit through this system. Since tokens of bad students will be the cheapest in the free market, the highest upside will be found exactly there. This will encourage teachers, mentors and investors to bring as many under-supported students as possible on the right track because it is not only the right thing to do but also financially lucrative.  Human micro-company This concept very much sounds like the venture capital (VC) world we live in today. And rightly so, the system has proven to be very successful for our economy and therefore also our society. Why wouldn’t it be successful if every human is seen as its own micro-company? VC firms are fantastic in scouting talents. They have a tremendous understanding of who has the right skill-set to build a startup and what teams and ideas might succeed. Not only provide VC firms funding for those startups, they support them through various ways over many, many years. They push teams hard and demand a lot from them. They manage to make good teams even better but at the same time are also there with support and ideas if things do not go as planned. VC firms have specialised in certain areas, meaning that some VC’s only invest in agriculture startups while others only invest in tourism startups because they are themselves experts in those fields. If we imagine a world in which every person has its own token traded on the public market then maybe new VC firms will be pouring huge amounts of money and resources into the education sector. The biggest beneficiaries might be exactly those schools or those young people that are off the radar right now and therefore start with a handicap into life. As mentioned above, the token prices of students in bad neighbourhoods and with a bad track record would trade significantly lower. Investments there would yield much higher returns and therefore VC firms could diversify their portfolio through investments into those students. Even a single investment in only one of the students would benefit the entire class and maybe even the school and neighbourhood. Because the learning of one individual can create a ripple effect within a friends circle or an entire class. Teachers and other people who are close to the most talented students will detect certain skills or a positive change in mind-set early and therefore can jump in before the professional VC’s do and therefore also financially benefit. This could again create a ripple effect, meaning that friends could encourage each other to do better in a certain field because their token price will go up.  Initial Token Launch The token could be programmed in various different ways to further incentivize certain social behavior. The initial token launch should be initiated by the government. At a very young age only teachers and other trusted members are allowed to acquire tokens of the child. This can easily be coded into the smart-contract. Once kids develop strong personalities and get old enough to make their own decisions the market should open for all participants. It’s important that mentors and investors can participate as early as possible since that support is critical at a young age. The issuer and holder of the token is the government. Once the public gets an opportunity to buy the tokens the government will earn money through the sale, which it can directly reinvest into the education system. It should even consider to redistribute a part of it back to the school of the child — therefore creating an even bigger incentive for the entire local school staff to do well. Dividends and pay-out Once the tax office is registering income by a person who was entered on the blockchain ten or fifteen years earlier during the creation of the personal token, money will be automatically distributed back to all token holders — therefore to all teachers, mentors and investors. This can be compared to a dividend as it is recurring income for all token holders every time there is a taxable event. It’s even possible that financial products would be created to increase speculation on the tokens, meaning that people could buy options to bet more money on the future outcome of someone. In most cases this should be positive for the individual as well as for society. Over decades, the market price of a token would go lower as people are slowly approaching the official retirement age. This again can be compared to a stock, which also goes through different periods — from a wild and highly speculative startup period to a more established and mature period in the public market. The price of a stock usually decreases when the outlook for future earnings sinks. The same will happen for tokens that are connected to a human identity and its income.  Downside

We have now seen some major benefits it could bring to our education system. It potentially is a new paradigm shift for our society and the biggest revolution in the sector. It would bring more equality and fairness to students. It would allow teachers and people in the education sector to financially benefit tremendously if they manage to shape a young human and bring them on the right track. It would maybe even motivate more people to become teachers since unlocking other people’s talents could be financially rewarding. But what about the downside of this system? As a society we do not only want to create a money driven workforce. We want to create a society that cares for each other, that is kind to each other, is peaceful and plays fair. Also, I am aware that not everybody is gifted with the same skills and talents at the point of birth. I am convinced that in todays world people can make it very far in life even when starting with a disadvantage. This new system would allow exactly those people to get the desperately needed support to accelerate in school and reach their full potential early in life. Reputation or voting system Almost everything can be programmed into a smart contract. We could discuss a reputation system that punishes bad actors, misbehaving or cheating. Or, we could discuss a system that benefits people who contribute to society with skills that are not always easy to monetize — think about artists, musicians or families. If we can agree that a person contributes positively to society than the early backers of that person should also benefit. A possible solution would be to redistribute some of the society’s gains to the early supporters. I do not have all the answers for potential flaws in this system. But I would like to trigger a conversation and read more thoughts from people in different fields and with different political views. Bottom line My feeling is that this new system allows millions of individuals to get much needed support faster, more direct and more early in life while the current education system completely lacks incentives for people working in the sector. Today, pupils and students are taught and treated as anonymous groups or classes and the results never have any positive or negative consequences for anyone who was part of their multi-year journey. Tokenizing the human potential would greatly benefit the entire spectrum of our society and therefore set the right incentives for teachers, friends, family or just anyone to help someone else develop skills. I am convinced it will have a dramatically positive effect on our society and for our country. Crypto and particularly smart contracts as well as the oracles that support them are not going away. We are about to see a rearchitecting of backend systems across all major industries. We all know this. But why does not everyone see the same?  First of all, because no one can predict the future. Even if something appears obvious to me or to you, there may be many other factors that start to play into it at a later point in time. But something became clear to me over the last few years I’ve worked in crypto. People who don’t see the transformation unfolding usually don’t know a lot about blockchain technology. I have yet to meet people who fully understand it and still don’t believe it will happen. We are about to enter a decade of tremendous change. But what is it that makes it so difficult to explain blockchain? Explaining blockchain to people requires a certain understanding of the history of money, the current state of technology, politics and even some imagination. But the single biggest problem is that there are almost none practical use cases. It’s not hard to explain the internet to people today. Pull out your smartphone and order some food. Book an Uber or an Airbnb. Open Facebook and contact someone on the other side of the world. You can even watch a live stream at the top of a mountain — with only a click of a button. But there aren’t yet any kind of end user applications that everybody is using on the blockchain. So we have to explain it theoretically. It’s almost like the internet in 1991. Back then, the internet technically worked but there simply wasn’t a popular web browser like Chrome or Internet explorer. There wasn’t a popular email service provider like Outlook or Gmail. It was very hard for people to imagine the effect it would have on their lives. Not even people working in the tech industry could see the full impact it would have. But some people realized that something was about to change. Today, I believe, we are again at the very same point in time. When we try to explain Blockchain to people we have to start with Bitcoin, because it started the whole movement of a decentralised web. It was the first use-case on the blockchain, but unfortunately for us the game-changer lies rather under the hood. Most people simply don’t care if a central bank sends the payment from my wallet to the other person’s wallet — or if thousands of computers do it simultaneously. Unfortunately, the word “Bitcoin” turns off so many people because most of them just see it as money. Speculative, non existing, evil money with nothing “real” backing it. There is this awkward gap that exists between the people who get it and the people who don’t. It almost seems like we don’t have a common language anymore. That’s why I try to break it down in easier words.  Technically, there are two major things humans exchange with each other:

The main difference between information and value lies in its functionality. One can be copied, the other can’t.

However, value can be a lot more than just a digital money. It can also be stocks, options, real estate — and contracts. Basically everything that should only be at one place at a time — even if its value is very, very small. The Internet is the global standard for the exchange of information. Before that we had private networks. Those were already useful. You could email your colleagues, you could share files within your private network or your company’s “intranet”. But today, with the help of TCP/UDP, IP, HTTP and other protocols we’ve connected those networks together. That’s the internet we know today. That’s what makes it so interesting and so useful, because the entire world is on the same page.  Until recently, we didn’t have a standard for the exchange of value. That’s why it is so difficult to send money or other value outside of countries. And It’s also hard to exchange different kinds of value with each other. Or buy or sell only a small percentage of a house — or trade a fraction of a famous Picasso painting. This is because the databases are not connected to each other. People have to manually check if you really own the house on one database, and manually check on another database if you really have transferred the money to the correct destination address. If money or value is sent from one person to another — we always need one or multiple middleman services because we can’t just trust each other. Banks have helped us for a long time, but the entire system operates like private networks. In the last decade more and more private tech companies tried to improve the system through the use of the internet but eventually still just created their very own networks and databases for transferring value. Lawyers and notaries also perform middleman services during sales processes. What we actually could need is some kind of global database — a ledger — that will keep track of all those activities so that everyone is on the same page. Just like the internet. And that is what we have today with blockchains. The world’s first decentralized database that nobody controls alone and everyone can access. Instead of one computer verifying a transaction and checking if there is enough value in your account to execute the transaction, thousands of computers do it at the same time. Not one person or one company controls the database but thousands of computers do so all over the world.  This makes it impossible for bad actors to cheat — or at least on the blockchain itself. Code is law. Everybody can use it, everybody can connect to it. No matter if you send a billion dollar or a single cent. No matter if you are rich or poor. No matter in which country you are or what kind of value you send. The blockchain is just like the internet, but this time it’s not for information but for value. Bitcoin — some years ago — was seen as some kind of decentralised internet money. Everybody could send money from point A to point B without a bank in the middle of the transaction. Fascinating. But this was just the beginning. Today, it is more seen as digital gold and therefore as a store of value. A few years after Bitcoin, Ethereum invented so called “Smart Contracts”. It allows users to send all kinds of value from point A to B. Think about all the financial products that exist today, shares, options, loyalty points, user generated currencies or complex contracts in venture financing. Think about your house in your country’s land registry database. It should only exist once. That’s value that you own. And that became-technically-transferable. Think about the hundreds of different databases your government uses right now. And all the databases of private companies. They are all controlled by central parties. In developed countries you can more or less trust them. If you buy a new house they will write that down in their own database. Yes, it might take weeks and will cost a lot of money but eventually it will be written down. But in many parts of the world this is a huge problem. The bank might refuses to send out the money to the destination you want it to go. Or the bank doesn’t send it as fast as you want it to be — even though it is your money. What if some people inside a corrupt government don’t want you to own the house anymore? They will just delete the entry of that database, or change it. It will be hard to proof it. The truth is not in your hand, but in the hand of a central player. This is the problem. They are controlled by someone else and they are not connected to each other. For end-users the consequence is that the process on them is usually slow and expensive. Removing the middleman from the database has very, very deep implications for our society. It means that suddenly the world connects. You can transfer value within seconds with no central party stopping it. Suddenly, you can trade stocks for real estate — or options for art — with everyone in the world.  But it also means that in a first move responsibility goes from central parties to end-users. And this is where many end-user applications will be needed to bridge it somehow.

But behind those applications will be a growing global decentralised database — a blockchain — that makes the transfer of value (whatever this may be) fast, cheap, instant and secure. Removing the middleman means that, technically, we don’t need Uber anymore, because what the company does is connecting two users to each other on a central database. Google and Facebook, who both earn a lot of money through collecting data from users and sell it to advertisers, could technically be replaced through different blockchain applications. All of those online services are just a middleman service. The bank that sends money from one account to the other account is also not needed anymore. This doesn’t mean that just everything disappears but that new things will be created. Banks will do consulting or find other fields to generate revenue. There still needs to be customer support for online services. And you can not let all people handle financial services on their own. But behind the scenes many things will get a lot easier, faster and cheaper — and decentralised. If this is going to unfold like I imagine it today, then we are going to see huge companies either die or transform into something entirely new. Entire industries will be transformed because most middleman services for online businesses will be facilitated through the blockchain. The single biggest losers in this decade of transformation could — ironically — be the tech companies themselves, unless they once again adopt to the new world. We are about to see a rearchitecting of backend systems across all major industries. We all know this. But why does not everyone see the same?