anuary 13th, 2025

Andrin Renz

6300 Zug,

Switzerland(Minority Shareholder)

Dear Fellow ODH Shareholders,

Before you make a decision, ask yourself: Is CHF 5.60, representing a 335 million market cap and 600 million enterprise value, a fair price for a company with billions in assets and stable, growing cash flows? For most of us, the answer is a clear “No.”

The timing could not be worse for selling the shares at such a low price - likely the very bottom. A turnaround in the stock price is long overdue and potentially inevitable once the company begins paying dividends, providing investors with real cash instead of reinvesting everything back into infrastructure and city building.As a long-time investor in this company,

I must raise my concerns about the tender offer by LPSO Holding Ltd., owned by the Sawiris family, to acquire our shares at CHF 5.60 per share - or, more precisely, about the risk of a potential squeeze-out.

The infamous CBRE report that went unnoticed

In 2018, a valuation by CBRE Group Inc. estimated the undeveloped land in El Gouna alone at USD 1.82 billion (!), nearly 170 times its book value. Yet, today, ODH’s market capitalization stands at USD 335 million, a fraction of its true worth.

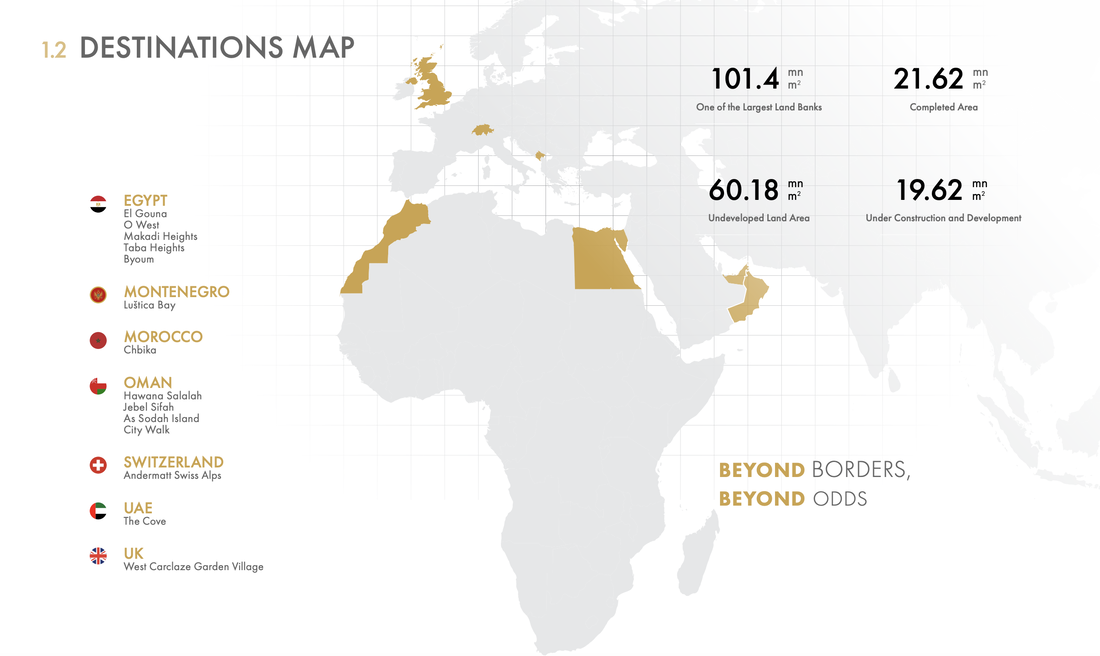

Orascom Development operates 10 destinations across 7 countries, including Egypt, Oman, Montenegro, Switzerland, and the United Kingdom. The CBRE report was just about the land of a single portfolio destination. In total, the company is sitting on 100 million square meters of premium land - an area roughly the size of Paris.

The company's assets include not only land, but also hotels, marinas, golf courses, residential communities, a hospital, super markets, sports facilities and even an airport and a football stadium.

This isn’t just undervaluation - it’s one of the most striking mispricings I’ve encountered. I ask all investors to please take a second look at Orascom's assets and help me push the market for a fair valuation and demand from the board a second fairness opinion - and at all costs - to prevent the squeeze-out.

After years of planting, the harvest is left behind.For years, ODH has strategically reinvested its profits from one destination into building entire towns from the ground up in new locations. In my opinion, this was a strategic decision I could support.

Developing a city to reach critical mass typically requires 10–15 years of substantial infrastructure investment. For a city to thrive and become as profitable as El Gouna in Egypt, it must reach a point where it provides a comprehensive range of infrastructure, services, shops, and activities to support a vibrant community and attract visitors, real estate buyers, and businesses.

Once this critical threshold is achieved, the city has the potential to transform into an unstoppable cash cow.In the early stages, some services need to be financially supported or subsidized to address the lack of infrastructure and amenities necessary to attract residents, tourists and businesses. However, as the population grows and the city becomes more established, the dynamic shifts - businesses want to be in the area and capitalize on the opportunities.

I am convinced that following this long-term strategy of reaching critical mass more quickly was the right approach, and therefore, instead of paying dividends, sending cash from one destination to another was the right thing to do. However, not if we are squeezed out at rock-bottom prices, causing all the money invested in infrastructure and the resulting land appreciation to be simply ignored.

The magic of the business model

What many investors and even analysts don't understand is the core of the business model. Orascom is not just a normal real estate developer. The enormous land bank was once purchased only for symbolic prices because it was in a remote location and has now - thanks to all the infrastructure - massively appreciated because it is no longer remote, empty land but is situated right next to vibrant, newly developed cities.

The long-term vision of Samih Sawiris and Orascom is genius, and I fully support it. However, as the CBRE report has shown, all the assets and the land bank are not adequately reflected in the books; we could potentially witness one of the biggest stock recovery stories on the Swiss stock exchange once other investors recognize the undervaluation of the land bank and the assets.

However, we must prevent ourselves from being squeezed out.Orascom has started building multiple new destinations in different countries around the same time, 15-20 years ago. Many towns are now already beginning to contribute positively to the group’s financials. Why sell now, when we are so close to realizing the full potential of those new cities?A premium that hides the real value

At first glance, CHF 5.60 might seem attractive:

- 40.7% premium over the 60-day average price.

- 38.3% premium over the last closing price before the offer.

But let’s be honest - a 40% premium on an already massively undervalued price still leaves us far, far, far below the true intrinsic value of our shares.For a deeper analysis of ODH's valuation, I encourage you to review my two detailed research reports:

- Blog 1 (2019): “Orascom owns assets in the billions, while its enterprise value is only in the millions.”

- Blog 2 (2024): “The undervalued share price of Orascom Development (an Update 2024)”

If you're interested in challenging my assumptions, sharing insights, or contributing in any meaningful way, I encourage you to get in touch with me.What can we do?

- Reject the offer (most important) to prevent a squeeze out!

If you believe in the long-term value of ODH, do not tender your shares.

- Request a second fairness opinion

Shareholders can demand the preparation of a second fairness opinion. I am in the process of doing it right now! Please join me.

- Collective action

Reach out and engage with fellow minority shareholders — together, our voices carry more weight, and we might be able to keep the stock listed.

- Stay kind, honest, and supportive

Let’s continue to support Orascom and the Sawiris family in building the most amazing towns and destinations

Reach out via:www.never-stop-asking.com/communityEmail: andrinrenz23@gmail.comSincerely,Andrin RenzMinority Shareholder

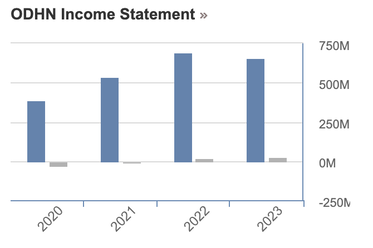

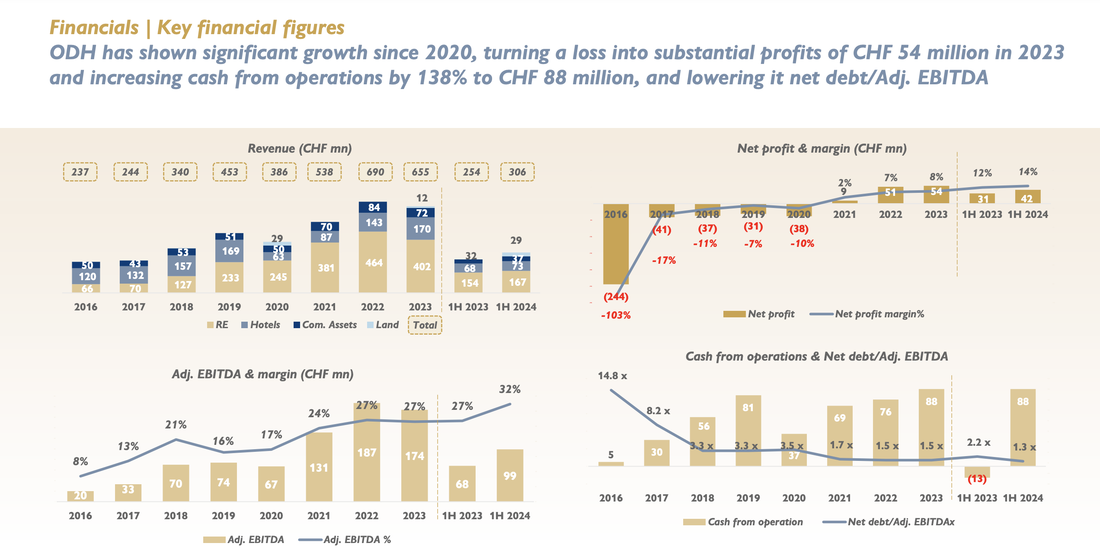

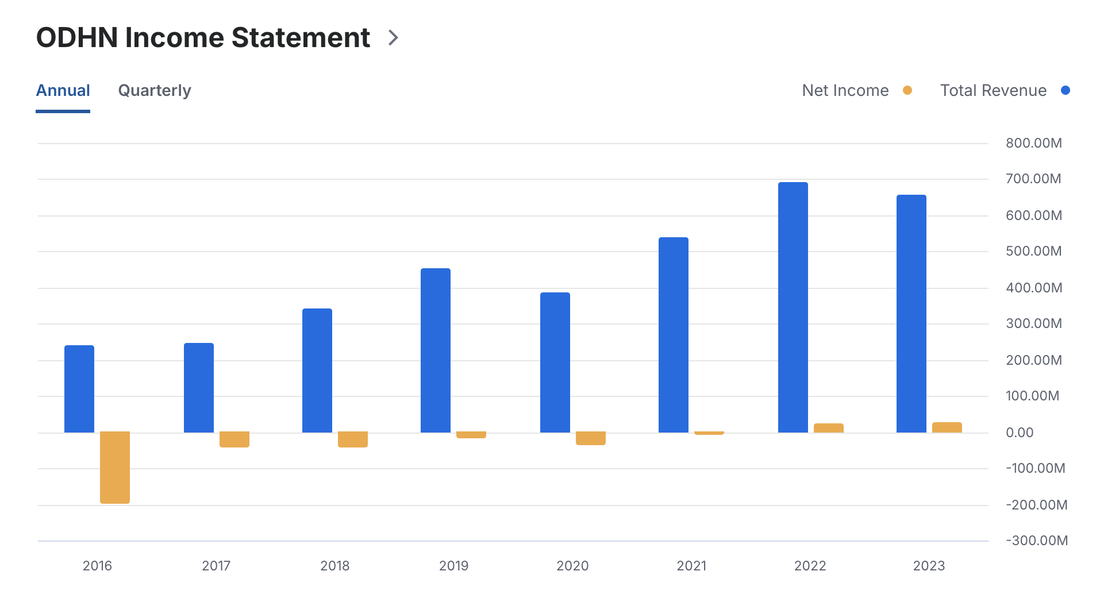

A Glimmer of ProgressBetween 2020 and 2023, however, ODH showed improvements:

- Revenues: Up 70%

- Adjusted EBITDA: Up 160%

- Net Profit: From a CHF 38 million loss to a CHF 54 million profit

Despite these improvements—which, for transparency, began at the pandemic's lowest point—the company remains only marginally profitable, as shown in the chart below. The blue bar represents revenue, while the gray bar shows profit or loss.

The devaluation of the Egyptian pound is frequently mentioned as a major challenge, often eroding significant portions of their operational profits. I just wish they would take a more active approach to hedging against it. That said, given their profitability, I’m surprised the share price has dropped even further since my last research report. While I still believe the company is massively undervalued—now even more so than five years ago—let’s dive deeper into the numbers and facts:

- Founded: 1989 (35 years in operation)

- Land Bank: Over 101 million m² (41% developed or under development)

- Operating Destinations: 11

- Hotels: 33 premium hotels with over 7,000 rooms

- Stock Listings: Swiss Stock Exchange (ODH), Egyptian Stock Exchange (ODE)

- Ownership: Sawiris family owns 76.4%; 23.6% is free float

- Core Revenue Segments:

- Real Estate (55%)

- Hotels (24%)

- Commercial Assets (12%)

- Land Sales (10%)

The Value GameIn 2018, CBRE valued land in El Gouna at CHF 80 per square meter. By 2024, ODH sold land at CHF 200–250 per square meter. Let that sink in. Despite these gains, ODH’s market cap remains shockingly low, even lower than ODE's, which ODH almost entirely owns.If there's a flaw in my thinking or the numbers, please let me know. I encourage you to fact-check and share your insights in the comment section below.

Debt and LiquidityOrascom currently has a total debt of CHF 470.2 million and cash reserves of CHF 197.5 million, resulting in a net debt of CHF 272.7 million. This level of debt is manageable within the real estate sector, where companies typically operate with higher leverage.Debt/Equity: 1.08xFor every CHF 1 of equity, ODH has CHF 1.08 of debt.This is considered reasonable for real estate companies, where ratios can often range from 1.0x to over 8.0x, depending on the business model.Debt/Total Assets: 0.28xOnly 28% of ODH’s total assets are financed through debt.This is well below industry averages, where 50%-60% of assets are often financed with debt.Net Debt/Adjusted EBITDA (Long-Term): 1.35xODH’s net debt is only 1.35 times its earnings before interest, taxes, depreciation, and amortization

.A ratio below 3.0x is generally considered healthy in the real estate sector, indicating that the company generates sufficient earnings to comfortably service its debt.These metrics show quite a strong liquidity and debt management. However, it’s worth noting that ODH completed a capital increase in April 2023, which definitely contributed to their improved financial position.However, it’s also important to note that their books contain significant hidden value, which could - on the other hand - improve some of the metrics mentioned above.That forms the core thesis of this research report.

What Is the Core of Their Business?Orascom has a magical yet simple business model: they build entire towns from scratch.

Their strategy is straightforward:

Step 1:They acquire VERY large tracts of very cheap land in remote areas (through government agreements)

Step 2:They develop key infrastructure, hotels, and real estate and much more.

Step 3: They develop entire towns, sometimes even with hospitals or sports clubs—for example in the town of El Gouna with the El Gouna Football Club, which competes in the top tier of the national league. In the same destination, they host cultural highlights like the internationally renowned El Gouna Film Festival or the El Gouna International Squash Open, a major tournament that attracts the world's top-ranked players. Alongside these, they have hosted Ironman competitions (for example in Hawana Salalah) and other world-class events in their various other destinations.

Basically, they offer everything you’d expect in a fully functioning 'normal' city.Step 4: Now, even after years of "city building," they still hold extraordinary amounts of empty land, much of which could now be sold at significantly higher prices.

This land remains recorded in Orascom's books at its original, much lower valuations, representing an unprecedented hidden reserve of potential value. That's exactly why I believe so much in the company and in the share price. However, feel free to challenge me here.

Harvesting the rewards

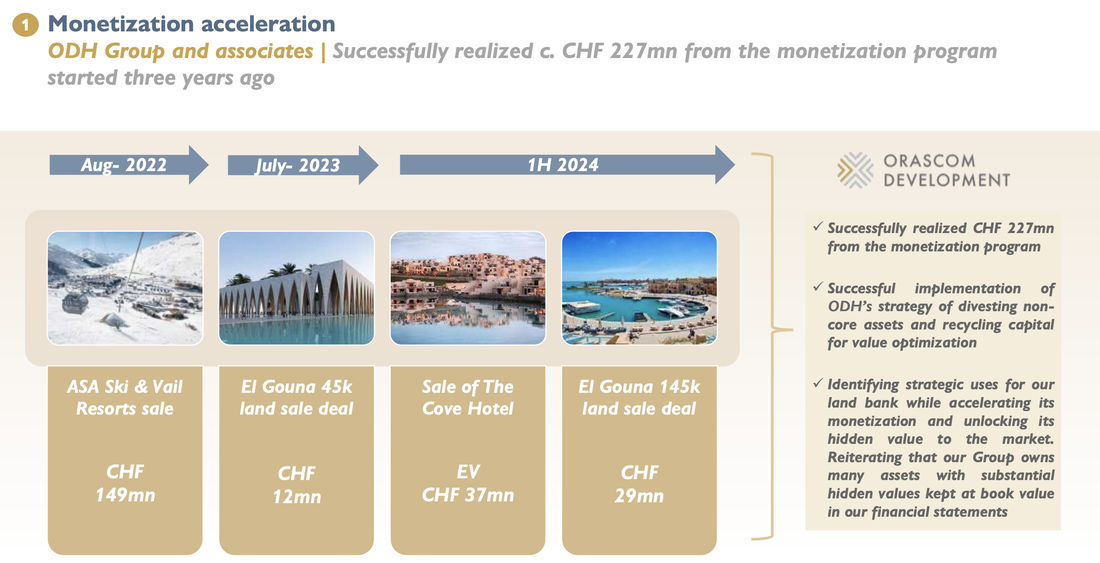

In my last research report, I predicted that the share price would rise once the company announced plans to actively monetize its land, such as through sales to third parties or joint ventures.

For years, founder Samih Sawiris avoided selling land to third-party companies, even though it could have generated quick and easy profits. He believed that selling would mean losing control over parts of the city—control that is essential for managing and maintaining a unified destination. I agree—having full control over the city ensures far greater efficiency. Selling off pieces weakens the unique advantages of private cities compared to government-run ones, where many stakeholders and competing interests often complicate progress.However, with the substantial rise in land value and the maturity of their destinations, adopting a monetization strategy now seems logical. Joint ventures or strategic land sales could allow Orascom to finally reap the rewards of years of restraint.

If the price is right—like in the case of El Gouna—they might even unlock this value while retaining overall control.My thesis was that once Orascom’s management announced this strategic shift, investors would recognize that the "hidden value" in the company’s books was no longer theoretical but about to be converted into real cash—possibly paid out as dividends. I expected this to generate significant investor interest, given Orascom’s vast land holdings and the potential to sell parts for hundreds of millions, or even billions, providing swift cash flow to investors.As I mentioned earlier, they announced this strategy change 2–3 years ago. Yet, surprisingly, the share price dropped...

What Makes Orascom Different Compared to Other Real Estate Developers?Building Entire TownsUnlike most developers who focus on single resorts, Orascom creates fully integrated towns (!) with residential areas, commercial spaces, hotels, and infrastructure. These are designed as self-sustaining communities. El Gouna, their flagship destination, has 25k (!) permanent residents and is still growing... three is still empty land. Strategic Land DealsOrascom secures very large amounts of land at very low costs through government agreements.

This is possible thanks to the Sawiris family’s strong connections and their proven success with projects like El Gouna. Ultra Long-Term VisionWhile many developers aim for quick profits, Orascom holds onto undeveloped land not for years, but for decades, allowing its value to increase as their towns grow and mature.Diversified IncomeOrascom doesn’t rely only on property sales. They earn steady revenue from hotels, retail spaces, and land sales, essentially collecting a “private tax” within their towns.

To put it into perspective:Orascom’s land reserves—100 million square meters—are similar in size to Paris (about 105 square kilometers) or Barcelona (around 101 square kilometers). Of this, 60.2 million square meters remain undeveloped, making up about 40% of their total land bank and offering huge potential for growth in the years ahead.Instead of being concentrated in one location, these reserves are spread across seven countries, which helps reduce risks. If political or economic issues arise in one country, cities in other regions can help balance out the losses.

The Bottom LineIt’s dark outside now in my coworking space in Vietnam, and it’s time to wrap this up. I still believe Orascom Development Holding (ODH) is a company full of potential but somehow stuck in a frustrating cycle.Every few years, they face a crisis—a tragedy, a pandemic, or another black swan event. After the Arab Spring, they tried to diversify their portfolio and push the other destinations much more, but it takes decades to build an entire town from scratch - or at least to a size in which it is profitable.

Keep in mind, the first few years of building the core infrastructure for a new town require a massive investment, and selling real estate is challenging when the town lacks basic amenities. However, once the difficult first decade is behind them, the profitability tends to grow exponentially. Now, there are several destinations that are self-sustaining or on the very brink of it. It's a very interesting point in time.

Despite owning billions in valuable assets and showing significant improvements, the market doesn’t seem to recognize their true worth—yet. Or perhaps that’s precisely the issue. Operating in markets like Egypt and Oman likely comes with a valuation discount, but how much of a discount is fair? That's up to the free market to decide. Challenges such as currency devaluation, past setbacks, and a lack of investor confidence have kept the stock undervalued. T

hese factors will likely continue to weigh on the company until it demonstrates consistent profits and sustainable, growing dividends.However, with a massive land bank, diversified projects, and steady progress in their core business, ODH has all the pieces in place to succeed.As their destinations mature, ODH will become more resilient to localized crises. More than ever, I believe we might be closer to a turnaround than most people think.If you enjoyed this research, please don’t hesitate to leave a comment, and feel free to challenge any part of my thesis or point out anything I might have missed.

.svg)